Madhuchanda DeyMoneycontrol Research

Highlights:

- Strong quarterly performance from Ujjivan Financial

- Healthy growth in assets and deposits

- Interest margin maintained

- Asset quality improves

- Despite regulatory overhang, the undemanding valuation deserves attention

-------------------------------------------------

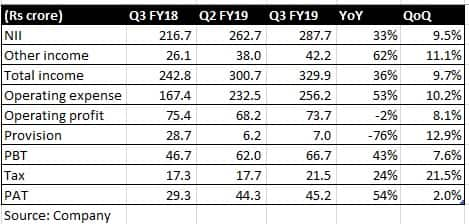

Against the backdrop of stock underperformance due to Reserve Bank of India's (RBI) diktat, the financial result of Ujjivan Financial was something to cheer investors with a 54 percent year-on-year growth in after tax profit.

Key positives

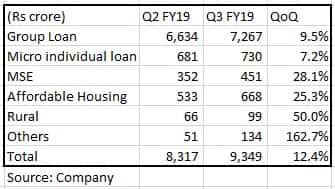

Strong performance on the business front: 32 percent YoY growth in assets under management (AUM) to Rs 9,349 crore and 35 percent growth in disbursement to Rs 2,885 crore.

Growth in disbursement as well as loan book was driven by small and medium enterprises (SME) as well as affordable housing. In SME, the non-banking financial company (NBFC) is shifting the loan book in favour of secured lending.

Efforts to de-risk and diversify the loan book is on. Growth in micro-finance, at 21 percent, was lower than the company average. The non-microfinance book surged 220 percent (albeit on a small base) and constituted 13.4 percent of overall portfolio compared to 5.5 percent a year back.

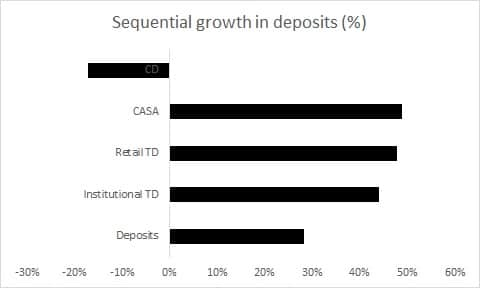

Its liability profile is improving, with steady accretion to deposits. While overall deposits showed a sequential growth of 28 percent, low-cost CASA (current and savings account) grew 49 percent and formed 10.4 percent of total deposits. At present, close to 58 percent of advances are funded by deposits as against 35 percent a year back. The bank is working on converting its asset customers to deposit holders and is targeting a CASA share of 30 percent in the next few years.

Source: Company

While the loan book is moving towards more secured lending (depressing yield on advances), thanks to the ramp-up in deposits (leading to a softening in the cost of funding), Ujjivan was able to maintain its interest margin at 11.8 percent.

Asset quality improved, with gross non-performing assets (NPA) declining to 1.4 percent from 1.9 sequentially. Net NPA stood at 0.3 percent, with provision cover (provision against NPA) at 81 percent.

Ujjivan is well capitalised to take advantage of the emerging opportunities, with capital adequacy ratio at 22.1 percent, much above the regulatory requirement. It is raising Tier II capital to boost its capital position further.

Key negatives

Cost-to-income ratio is still high (77.7 percent) as the management continued to rollout branches and boost its headcount. It added 97 branches in Q3, taking the total number of banking outlets to 464. The pace of addition is certainly going to decelerate in FY20. As the bank starts sweating these assets efficiently, it is looking at substantial moderation in the cost-to-income ratio to 50-55 percent over the next three years.

While farm loan waivers so far hasn’t had any impact on its overall business, the management alluded to challenges in a small pocket of Madhya Pradesh on account of the same.

Other observationsUjjivan is confident of asset growth upwards of 35 percent in the current fiscal. It has identified three candidates for the position of Managing Director, which will be sent to RBI shortly.

To meet with the licencing norms (listing of the bank by January 2020 and paring down promoter holding to 40 percent by January 2022), the management is working on a number of alternatives and will initiate discussion with RBI and the Securities and Exchange Board of India (SEBI).

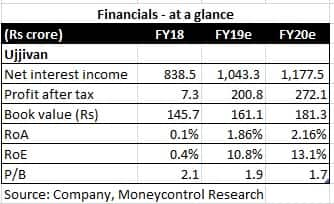

OutlookImprovement in the liability mix and diversification of asset book would continue to de-risk the business without comprising much on profitability. Moderation in cost-to-income ratio will provide significant boost to medium-term earnings. After the demonetisation blues, asset quality stress is largely behind. While the regulatory overhang pertaining to listing the small finance bank remains, correction in the stock price (down 30 percent in the past one year) has rendered valuation undemanding (1.7 times FY20 estimated book) in the context of its future prospects.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!