")

Anubhav SahuMoneycontrol Research

ITC’s third quarter headline numbers were tad below consensus but segments like FMCG and hotels performed on expected lines. With uncertainty over GST rates for cigarettes over, budget announcements focused on the rural economy could be the next trigger for ITC’s other lines of business.

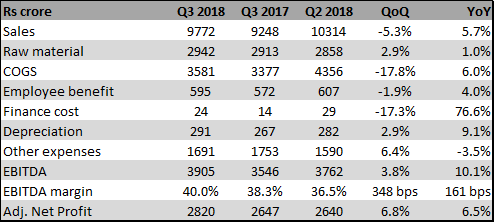

Q3 results: improved margins

While topline numbers were slightly below expectations, adjusted net profit was close to expectations. Net profit, if adjusted for exceptional item concerning Tamil Nadu entry tax, amounted to around Rs 2800 crore, up 7% quarter-on-quarter. This was possible due to better margins. EBITDA margin was about 40% vs. 38.3% in Q3 2017.

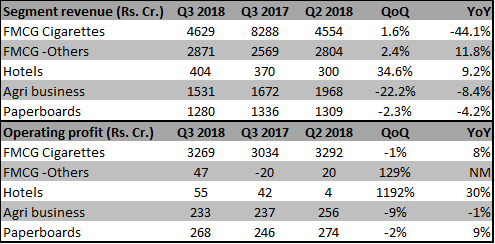

Segmental business: FMCG scaling up

As expected, cigarette business was impacted by lower volumes. Sales in the hotel business rose 9% year-on-year and operating profit was up 30%, in-line with sector wide trend. FMCG business topline numbers were up about 12 percent YoY. Its operating profit doubled sequentially, underlining the improving trend.

Budget is the next trigger

ITC remains a value play. Its P/E multiple is at multi-year low compared to industry leader and sector average. Stock currently trading around 32 times trailing earnings vs 58 times for HUL.

There FMCG business is showing improving results in terms of profitability and remains well positioned to benefit from vertical integration and investment in supply chain. Further, on the key cash flow business, cigarettes, worst of tax related headwinds seems over.

With Budget is around the corner, in the year of state elections, announcements pertaining to improving farm income, food processing industry, investment on rural infrastructure could be positive for the stock.

@anubhavsays

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!